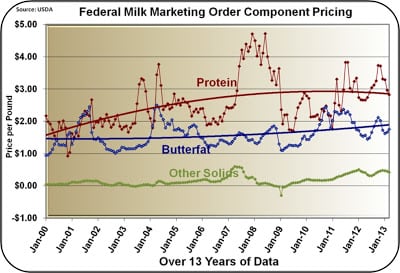

The Class III price fell 2% from $17.25 per hundredweight (cwt) in February to $16.93 per cwt in March.

This was due to a 1% drop in the National Agricultural Statistics Service (NASS) price for cheese and a 5% drop in the price of dry whey. Class III milk prices are driven by cheese prices.

The long term trends for component pricing are not significantly changed. Inventories of cheese, butter, and dry whey were all higher at the end of February.

Any real recovery in component prices will depend on a reduction of these inventories.

One of the major changes causing inventory fluctuations is the changing consumer consumption patterns of US customers.

The changes are influenced by retail prices and new dairy products that are changing the eating habits of US customers.

Cheese consumption and retail pricing

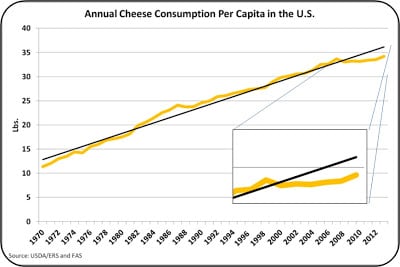

US domestic consumption of cheese and cheese products has shown a steady increase for over 40 years.

Per capita consumption has been the driver, and this consumption rate is still well below European levels, so the growth has been expected to continue.

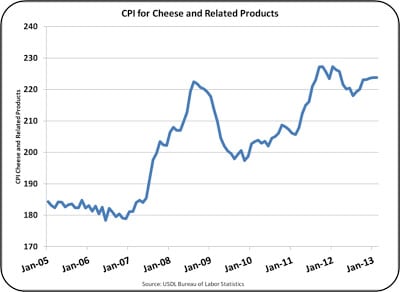

However, starting in 2007 there was a softening of that growth. There was still some growth, but it was much slower than the long term trend. Two things happened in 2007; the U.S. recession, and increased retail prices for cheese.

Pricing took a 20% jump between 2007 and 2009.

Although there was some easing of prices in 2010, retail prices continued climbing, especially in 2012. The early data for 2013 shows a leveling (no decrease) in retail prices, but these early numbers are also subject to change.

The conclusion seems to be obvious.

The main driver of milk prices in the US, cheese, has taken a hit.

When this happens, the supply of whey will also decrease. With these reductions in supply, prices for cheese and dry whey will improve.In the long term, this can create two changes which will impact Class III milk prices. The drop in demand for cheese has increased inventories and depressed the cheese price. Production of cheese will have to be reduced.

This will positively impact both milk protein and other solids prices, and increase the Class III milk prices.

Butter....

Per capita domestic consumption of butter is up slightly after a 30 year flat run.

Butter substitutes were developed in the 1930s and were expanded during World War II. This drove butter consumption down nearly 75% and the consumption remained stable for the next three decades.

The pricing for butter has fluctuated, but has actually decreased a little since reaching a high in mid 2011.

However, the increased consumption does not seem to be related directly to pricing.

However, just in the last few years, butter consumption has started to increase to levels not seen since the 1970s.

US-based John Geuss (pictured) is the editor of US dairy commodities blog, MilkPrice.

For more of John's in-depth month-to-month dairy commodity price updates, click here.