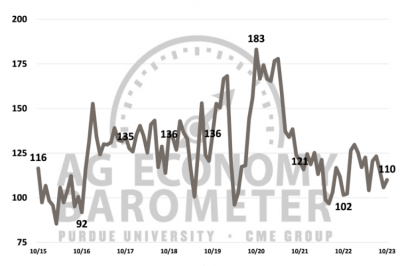

US: Farmer sentiment rallies in November 2023

The Purdue University-CME Group Ag Economy Barometer climbed five points to reach an index value of 115 which left the index 12 percent higher than a year earlier.

A 12-point increase in the Current Conditions Index was largely responsible for the improvement in sentiment, while the Index of Future Expectations also improved by 2 points. Year-on-year, both sub-indices increased – the Current Conditions Index rose 15% and the Future Expectation Index was up 11% on November 2022.

Responses for the latest survey were collected the same week that Congress passed an extension of the 2018 Farm Bill, i.e. November 13-17, 2023.

The Farm Financial Performance Index also improved, by 3 points, to move to 95 points, its highest reading of 2023. The index, which is based upon a question that asks producers to compare their farms’ financial performance this year to last year, was 10% higher than at the outset of this fall’s harvest in September and up 25% compared to its lowest point of 2023 back in May. Comparing responses received in May to those in the November survey highlights the change in producers’ perspectives about farm income. When comparing the two surveys the biggest shift was movement toward expecting financial performance to be about the same as last year and away from expecting worse performance than a year ago. In November just 22% of respondents said they expected worse financial performance than a year earlier whereas in May the percentage expecting worse performance was 38%. At the same time, the percentage of respondents expecting financial performance to be about the same as a year earlier rose to 61% in November from 48% who felt that way in May.

The Farm Capital Investment Index, which has ranged from a high of 45 in July to a low of 35 in October, rose 7 points to a reading of 42. 16% of respondents perceived the present time as good for large investments, almost on a par with July’s high point of 17%, with ‘higher dealer inventories’ the top choice as to why (chosen by 29% of the respondents). This could be a sign that farm equipment prices are starting to ease, authors James Mintert and Michael Langemeier of the Purdue Center for Commercial Agriculture noted.

Higher input costs, rising interest rates and the lower crop and/or livestock prices were the biggest concerns for producers in the year ahead.

Short and long-term farmland value expectations changed little month on month. The Short-Term Farmland Values Expectation Index remained unchanged at a reading of 125, while the long-term index dropped back by 5 points to a reading of 151. The short-term index has been in a range of 125-126 since June, while the long-term index has been in a range of 151-156 over that same time frame. Over 80% of respondents who expect farmland values to rise over the next five years said the main reason for optimism is ”non-farm investor demand” (59% of respondents) or “inflation” (23% of respondents).